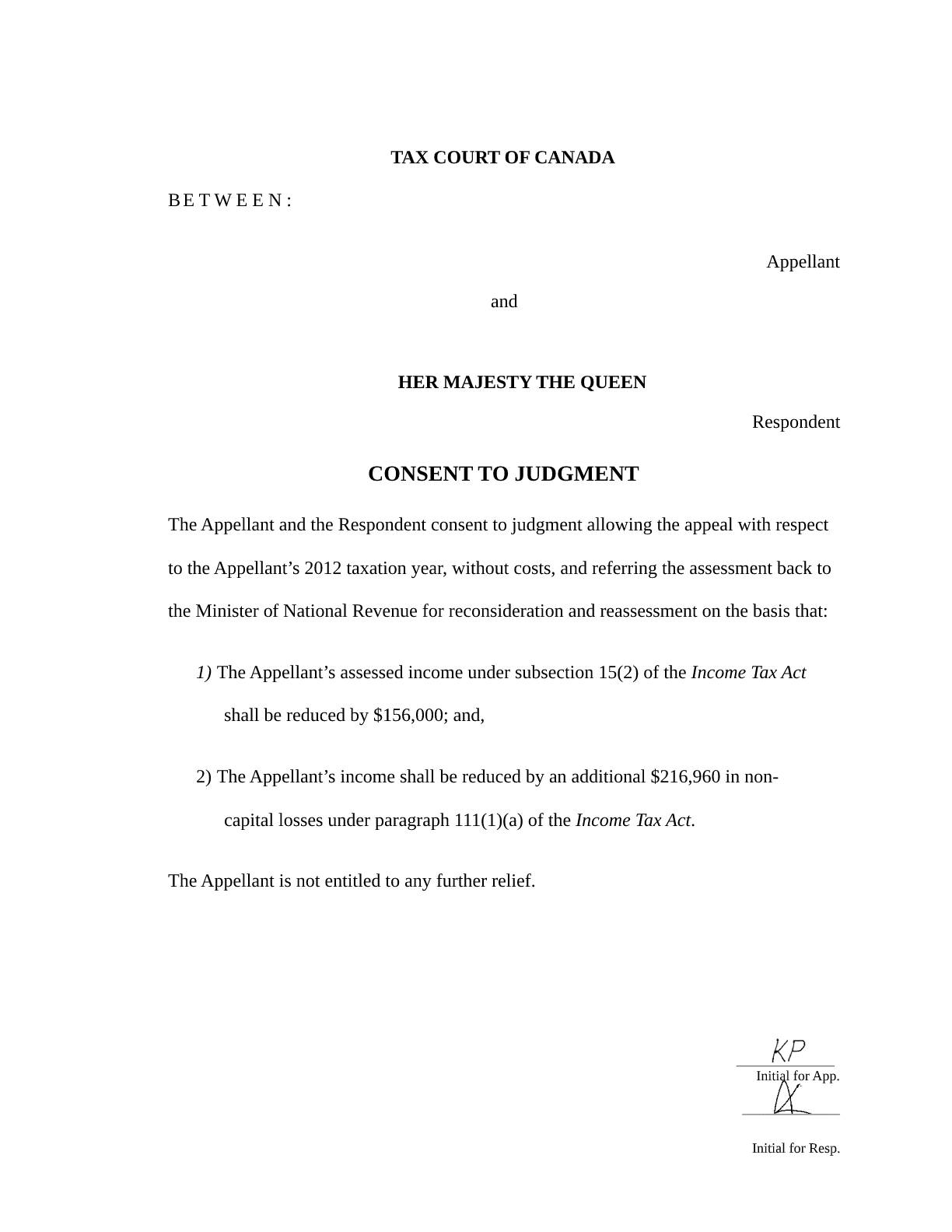

CRA Tax Audit, CRA Net Worth Assessment, and Tax Court of Canada Appeal Overview

A CRA tax audit can be stressful under any circumstances. The situation becomes even more challenging when a taxpayer has suffered a serious injury, faces a substantial tax reassessment based on a CRA net worth audit, and discovers that important procedural opportunities were missed during the early stages of a tax dispute.

This was the situation facing Mr. Pat Pizza (name withheld due to solicitor-client confidentiality). Before retaining TaxPage, Mr. Pizza had engaged another Canadian tax lawyer and accountant to deal with a CRA tax audit and subsequent Tax Court of Canada appeal involving his corporation. By the time TaxPage became involved, significant challenges had already arisen, including deficiencies in the pleadings, unanswered Requests to Admit that resulted in deemed admissions, and the failure to conduct discoveries relating to the CRA’s evidence.

TaxPage’s experienced Canadian tax lawyers were subsequently retained to address both the substantive tax issues and the procedural deficiencies that had arisen during the earlier stages of the dispute.

Despite these challenges, TaxPage successfully developed and implemented a strategy that ultimately reduced the corporation’s reassessed income from approximately $727,000 to approximately $310,000, eliminated more than $66,000 in gross negligence penalties, and generated overall tax and interest savings estimated at approximately $330,000. The matter was resolved without proceeding to a full Tax Court trial.

This case demonstrates the importance of retaining an experienced Canadian tax litigation lawyer when dealing with a CRA tax audit, CRA net worth assessment, gross negligence penalties, or a Tax Court of Canada appeal.

TaxPage’s approach in this matter reflects established Canadian tax litigation principles routinely applied in complex CRA tax audit and Tax Court of Canada appeal disputes, particularly where CRA net worth audit methodologies are challenged using contemporaneous transactional records and forensic accounting reconstruction.

CRA Net Worth Audit Lawyer Canada – TaxPage Representation in Complex CRA Tax Audit Disputes

TaxPage provides representation for taxpayers facing CRA net worth audits, CRA tax reassessments, and Tax Court of Canada appeals across Canada. These disputes often involve indirect income reconstruction, gross negligence penalties, and complex evidentiary challenges requiring experienced Canadian tax litigation counsel.

Our experience includes defending cash-intensive businesses such as restaurants, franchises, and owner-operated corporations where CRA audit methodologies rely heavily on assumptions rather than direct transactional verification.

What Does a CRA Net Worth Audit Lawyer in Canada Do?

A CRA net worth audit lawyer in Canada assists taxpayers in challenging CRA reassessments that are based on indirect income estimation methods rather than direct accounting records. These cases typically involve reviewing CRA assumptions, reconstructing financial data, challenging gross negligence penalties, and representing taxpayers in Tax Court of Canada appeals. Effective defence strategies often rely on forensic review of banking records, accounting systems, and point-of-sale data to demonstrate inconsistencies in the CRA’s reconstruction methodology.

CRA Tax Audit and CRA Tax Reassessment Background Facts

Mr. Pat Pizza owned and operated a pizza franchise through a corporation (“Pizza Corp”).

Following a CRA tax audit of Pizza Corp’s operations for the 2013 through 2015 taxation years, the CRA reassessed the corporation using a CRA net worth audit methodology. The CRA concluded that Pizza Corp had substantially underreported income and increased the corporation’s taxable income by approximately $727,000.

CRA tax audit determinations frequently rely on indirect assumptions rather than direct transactional verification, making contemporaneous financial records, POS data, and banking records critical in assessing the reliability of a CRA tax reassessment.

In addition to increasing income, the CRA disallowed various business expenses and assessed gross negligence penalties. The combined effect of the reassessments created significant financial exposure for both Pizza Corp and Mr. Pizza.

Unfortunately, the substantive tax issues were only part of the problem.

When TaxPage reviewed the file, it became apparent that several procedural opportunities had already been missed and that significant work would be required simply to place the taxpayer in the best possible position to challenge the reassessments.

CRA Tax Reassessment Based on a CRA Net Worth Audit

The CRA’s reassessment was based primarily on a net worth analysis that alleged substantial unreported income. Because net worth audits depend heavily upon assumptions regarding assets, liabilities, expenditures, and available sources of funds, a detailed review of the CRA’s methodology became essential to the taxpayer’s defence.

Procedural Challenges in the CRA Tax Audit and Tax Court of Canada Appeal Identified by TaxPage’s Experienced Canadian Tax Lawyers

One of the first steps undertaken by TaxPage was a comprehensive review of the existing litigation file.

That review revealed several significant procedural deficiencies requiring immediate attention. Before TaxPage became involved, key litigation steps had either not been completed or had been handled in a manner that exposed the taxpayer to unnecessary risk.

Deficiencies in the Notice of Appeal in the Tax Court of Canada Appeal

The original Notice of Appeal did not fully articulate the factual and legal basis upon which the reassessments were being challenged. TaxPage determined that amendments were necessary to ensure that the relevant facts, issues, and legal arguments were properly before the Tax Court of Canada.

Request to Admit Issues Affecting the CRA Tax Reassessment Appeal

A Request to Admit served by counsel representing the CRA had not been answered. As a result, certain facts became deemed admissions under the Tax Court of Canada Rules. Depending upon their nature, deemed admissions can significantly restrict a taxpayer’s ability to challenge aspects of the CRA’s position and may materially affect the outcome of a case.

Discovery Deficiencies in the CRA Tax Audit Litigation Process

Discoveries concerning the CRA’s assumptions, calculations, and supporting evidence had not previously been conducted. As a result, important assumptions underlying the reassessments had not yet been fully examined or challenged.

TaxPage immediately undertook a detailed review of the file, prepared an Amended Notice of Appeal, and developed a strategy designed both to challenge the CRA reassessments and to address the procedural issues inherited from earlier stages of the dispute.

This aspect of the case serves as an important reminder that retaining an experienced Canadian tax appeal lawyer at the earliest possible stage of a CRA tax audit or Tax Court appeal can often prevent costly procedural complications from arising in the first place.

Challenging the CRA Net Worth Audit Methodology and CRA Net Worth Assessment

A central issue in this appeal was the CRA’s reliance on a net worth audit.

CRA net worth audits frequently result in significant tax reassessments because the CRA reconstructs a taxpayer’s income using indirect methods rather than relying solely on the taxpayer’s books and records.

TaxPage has written extensively about CRA net worth audits and income tax gross negligence penalties. Readers interested in CRA tax audit defence strategies, CRA net worth audit methodology, and Tax Court of Canada appeal procedures may find these resources helpful in understanding how indirect income reconstruction is challenged in litigation.

This type of CRA tax audit determination often depends heavily on indirect assumptions rather than direct transactional evidence, making the quality and completeness of contemporaneous financial records critical in evaluating the accuracy of the CRA tax reassessment.

What Is a CRA Net Worth Audit?

A CRA net worth audit is an indirect audit method used when CRA auditors believe that a taxpayer’s books and records do not accurately reflect income. Instead of relying solely on reported revenues and expenses, the CRA attempts to estimate income by examining increases in assets and comparing those increases to reported income.

The CRA may also consider personal expenditures, liabilities, banking records, and information obtained from third parties.

Common Problems with CRA Net Worth Assessments

Although CRA net worth audits are commonly used by the CRA, they are often challenged because relatively small errors in opening balances, asset valuations, personal expenditures, shareholder loan accounts, or non-taxable sources of funds can produce significant distortions in the resulting calculations.

In many cases, taxpayers assume that the CRA’s calculations are based on direct evidence of unreported income. In reality, a net worth assessment often depends upon a chain of assumptions. If one or more assumptions are incorrect, the resulting reassessment may be significantly overstated.

Small errors in a net worth assessment can produce surprisingly large reassessments, particularly where the CRA’s assumptions are compounded over multiple taxation years. As a result, taxpayers should carefully review the assumptions underlying any CRA net worth audit and obtain advice from an experienced Canadian tax litigation lawyer as early as possible.

TaxPage’s Review of the CRA Net Worth Assessment

As part of its review, TaxPage carefully analyzed the assumptions underlying the CRA’s net worth assessment and identified several areas requiring further examination, including:

- The treatment of personal expenditures;

- The calculation of opening and closing net worth;

- The inclusion of certain assets and liabilities;

- The treatment of shareholder loan accounts;

- The treatment of non-taxable sources of funds; and

- The overall methodology used to estimate income.

TaxPage developed a counter-net-worth analysis to challenge the accuracy of the CRA’s assumptions and conclusions.

According to David J. Rotfleisch:

“Net worth audits remain one of the CRA’s most powerful audit tools, but they are far from infallible. Taxpayers should never assume that a net worth assessment is accurate simply because it was prepared by the CRA. Every assumption must be tested against the available evidence.”

As David J. Rotfleisch has also observed:

“A successful tax appeal often begins by identifying what the CRA assumed rather than what the CRA proved. In many reassessment cases, that distinction becomes critically important.”

The detailed review of the CRA’s assumptions provided the foundation for the litigation strategy that followed. The next stage of the appeal focused on gathering evidence, conducting discoveries, challenging the CRA’s calculations, and positioning the matter for a favourable resolution.

Evidence Gathering and Discovery in the CRA Tax Audit and Tax Court of Canada Appeal

Following the procedural remediation and initial review of the CRA tax reassessment, TaxPage focused on building a robust evidentiary foundation for the Tax Court of Canada appeal.

A successful challenge to a CRA net worth assessment depends heavily on documentary evidence capable of rebutting the assumptions used by the CRA. Unlike traditional audits, a CRA net worth audit relies on indirect reconstruction of income, meaning that the taxpayer must often reconstruct financial reality with precision and consistency to effectively challenge the CRA’s position.

TaxPage worked closely with Mr. Pat Pizza and supporting professionals to gather, reconcile, and organize the relevant financial records. This included corporate tax filings, banking records, point-of-sale reports, internal accounting records, and supporting documentation for both personal and corporate expenditures.

The objective was to establish a coherent evidentiary narrative that directly addressed the assumptions underlying the CRA tax reassessment and strengthened the taxpayer’s position in the Tax Court of Canada appeal.

Discovery Strategy in the CRA Tax Audit Litigation Process

Discovery played a central role in advancing the litigation strategy.

Given Mr. Pizza’s prior head injury and resulting cognitive limitations affecting memory recall, TaxPage adopted a tailored discovery approach to ensure accuracy, reliability, and fairness in the evidentiary record.

Instead of proceeding exclusively through oral examinations, TaxPage negotiated a structured written discovery process. This approach allowed the taxpayer to carefully review documentation before responding, reducing the risk of inconsistency while preserving procedural fairness.

At the same time, TaxPage conducted a comprehensive analysis of the CRA’s assumptions and evidentiary record. This included a detailed review of the calculations underpinning the CRA net worth assessment and identification of gaps in the evidentiary foundation relied upon by the CRA.

According to David J. Rotfleisch:

“Discovery in tax litigation is often where the true strength or weakness of a reassessment becomes visible. What is assumed during audit must withstand scrutiny when tested against the evidentiary record.”

TaxPage’s approach reflects established Canadian tax litigation standards applied in complex CRA tax audit and Tax Court of Canada appeal matters involving indirect income reconstruction.

CRA Tax Reassessment Settlement Negotiations Conducted by TaxPage’s Experienced Canadian Tax Lawyers

As the Tax Court of Canada appeal progressed, settlement discussions were initiated with counsel representing the CRA.

CRA Tax Audit Defence Strategy and Evidentiary Leverage in a CRA Net Worth Audit Appeal

Following review of the evidentiary record, the Canadian tax litigation lawyer acting for the CRA advanced an initial settlement proposal. While the proposal included partial concessions on income adjustments, it maintained the gross negligence penalties and did not adequately address key deficiencies identified in the CRA net worth assessment.

As the evidentiary record developed, the CRA’s settlement position evolved in response to increasing disclosure of franchisor-controlled POS data, banking reconciliation evidence, and consistent accounting records that materially reduced the reliability of the net worth reconstruction model.

Strategic Response to the CRA Tax Reassessment and Gross Negligence Penalties

TaxPage developed a structured counterproposal grounded in the evidentiary record and the legal standards governing CRA net worth audits and penalty assessments.

A key focus was the reliability of the assumptions underlying the CRA net worth assessment, particularly with respect to opening balances, personal expenditures, and classification of funds.

TaxPage also challenged the imposition of gross negligence penalties. As set out in TaxPage’s analysis of gross negligence penalties, the CRA must establish more than mere error or discrepancy; it must demonstrate the requisite level of carelessness or wilful conduct required by law.

Where certain documentation gaps existed, TaxPage adopted a targeted litigation strategy that prioritized the strongest evidentiary positions while maintaining credibility in settlement negotiations.

This approach significantly improved the taxpayer’s negotiating position and facilitated continued discussions with the CRA litigation counsel.

CRA Tax Reassessment, Gross Negligence Penalty, and Tax Liability Resolution

After sustained negotiations and continued advancement of the Tax Court of Canada appeal, the Canadian tax litigation lawyer acting for the CRA ultimately accepted the settlement terms advanced by TaxPage.

The resolution represented a substantial success for both Mr. Pizza and Pizza Corp.

The CRA agreed to reduce the reassessed income from approximately $727,000 to approximately $310,000.

The CRA further agreed to vacate gross negligence penalties exceeding $66,000 in their entirety.

Readers may also wish to review TaxPage’s detailed discussion of CRA objection procedures in relation to tax reassessments:

https://taxpage.com/articles-and-tips/notice-of-objection/

and Tax Court appeal processes:

https://taxpage.com/tax-appeals/

When interest savings were included, the total financial benefit was estimated at approximately $330,000.

Resolution of the CRA Tax Audit and Tax Court of Canada Appeal

By April 2026, the settlement was fully implemented and reflected in the taxpayer’s CRA account.

The Tax Court of Canada appeal concluded without the need for a full trial, demonstrating the effectiveness of early evidentiary reconstruction, targeted litigation strategy, and disciplined settlement negotiation.

According to David J. Rotfleisch:

“Effective tax litigation is rarely about a single argument. It is about building a consistent evidentiary and legal position that the CRA cannot sustain when fully tested.”

Reopening Personal CRA Tax Reassessments Through Strategic Tax Objection Planning

During the course of the corporate tax litigation, TaxPage identified additional personal tax reassessments issued against Mr. Pizza, exceeding $400,000.

These reassessments had become procedurally challenging due to missed objection deadlines arising prior to TaxPage’s involvement.

Strategic CRA Tax Objection Approach and T1 Adjustment Requests

After detailed review, TaxPage implemented a procedural strategy involving T1 adjustment requests designed to trigger fresh CRA reassessments.

This approach resulted in the issuance of new reassessments by the CRA.

Upon issuance, TaxPage immediately filed Notices of Objection challenging the reassessments in full, including associated gross negligence penalties.

Readers interested in the objection process may wish to review TaxPage’s article on the Notice of Objection process and Tax Appeals.

Preserving Taxpayer Rights in CRA Tax Reassessment Disputes

This portion of the case illustrates that procedural constraints do not always represent the end of a taxpayer’s rights.

In appropriate circumstances, procedural mechanisms may exist to reopen or reframe disputes, particularly where reassessments are reissued or materially altered by the CRA.

For Mr. Pizza, this strategy preserved the ability to challenge over $400,000 in personal tax exposure that might otherwise have remained unreviewable.

According to David J. Rotfleisch:

“Tax litigation is not only about substantive tax law. It is equally about procedural timing, strategy, and understanding how to lawfully reposition a file when conventional remedies appear closed.”

Lessons Learned from a CRA Tax Audit, CRA Net Worth Assessment, and Tax Court of Canada Appeal

This case provides several important lessons for taxpayers facing a CRA tax audit, CRA net worth assessment, gross negligence penalties, or a Tax Court of Canada appeal.

CRA Tax Audit Outcomes Depend on Evidence, Not Assumptions

A key takeaway from this matter is that CRA tax audit results are heavily dependent on the quality and structure of evidence presented. Where taxpayers can demonstrate consistent, verifiable financial records, the CRA’s ability to rely on indirect assumptions is significantly reduced.

This case illustrates that contemporaneous transactional records—particularly POS data, banking deposits, and accounting records—can materially alter the outcome of a CRA net worth assessment.

Procedural Issues in a Tax Court of Canada Appeal Can Materially Affect Risk

This matter also demonstrates that procedural missteps at the early stages of litigation can significantly increase risk exposure.

Issues such as deficient pleadings, unanswered Requests to Admit, and incomplete discoveries can constrain a taxpayer’s ability to fully challenge a CRA tax reassessment.

Retaining an experienced Canadian tax lawyer or Canadian tax appeal lawyer at an early stage can help ensure that procedural rights are preserved throughout the Tax Court of Canada appeal process.

CRA Net Worth Assessments Are Highly Sensitive to Assumptions

CRA net worth audits are inherently assumption-driven. As a result, they are particularly vulnerable to challenge where taxpayers can demonstrate inconsistencies in:

- opening balances

- asset valuations

- personal expenditure assumptions

- shareholder loan account treatment

- non-taxable source identification

Even relatively small adjustments to these assumptions can produce significant changes in assessed income.

Gross Negligence Penalties Require a High Legal Threshold

This case further confirms that gross negligence penalties are not automatic.

The CRA must establish a high evidentiary threshold before such penalties can be imposed. Where taxpayers can demonstrate reasonable reporting positions or evidentiary uncertainty, penalties may be reduced or eliminated.

For further discussion, see TaxPage’s article on gross negligence penalties:

https://taxpage.com/articles-and-tips/income-tax-gross-negligence-penalties/

Strategic Negotiation Can Resolve Tax Disputes Without Trial

Many taxpayers assume that a Tax Court of Canada appeal will proceed to trial. In practice, most matters are resolved through negotiation when properly prepared.

A well-developed evidentiary record, combined with disciplined legal positioning, often creates strong settlement leverage with counsel representing the CRA.

According to David J. Rotfleisch:

“In tax litigation, the best results are often achieved not at trial, but at the point where the evidentiary record forces a realistic reassessment of risk.”

CRA Tax Audit and Tax Reassessment Insights from an Experienced Canadian Tax Lawyer

Taxpayers facing a CRA tax audit, CRA tax reassessment, or Tax Court of Canada appeal should consider the following strategic principles.

Early Engagement of a Canadian Tax Lawyer Improves Outcomes

Early involvement of an experienced Canadian tax lawyer can materially improve outcomes by ensuring:

- proper issue identification

- timely procedural compliance

- preservation of evidentiary records

- strategic framing of disputes

Documentary Evidence Is Often Decisive in CRA Tax Disputes

The strength of a taxpayer’s case frequently depends on documentation rather than oral explanation. Banking records, POS data, accounting systems, and third-party confirmations can all play a critical role.

CRA Assumptions Must Be Actively Challenged

Taxpayers should not accept CRA assumptions at face value. Each assumption underlying a CRA net worth assessment should be tested against available evidence.

Objection Deadlines Must Be Carefully Managed

Missing objection deadlines can significantly restrict legal remedies.

For more information, see TaxPage’s article on Notices of Objection:

https://taxpage.com/articles-and-tips/notice-of-objection/

and Tax Appeals:

https://taxpage.com/tax-appeals/

What Does a CRA Net Worth Audit Lawyer in Canada Do?

A CRA net worth audit lawyer in Canada assists taxpayers in challenging CRA reassessments that are based on indirect income estimation methods rather than direct accounting records. These cases typically involve reviewing CRA assumptions, reconstructing financial data, challenging gross negligence penalties, and representing taxpayers in Tax Court of Canada appeals. Effective defence strategies often rely on forensic review of banking records, accounting systems, and point-of-sale data to demonstrate inconsistencies in the CRA’s reconstruction methodology.

CRA Net Worth Audit Defence Strategies Used in Tax Court of Canada Appeals, Frequently Asked Questions About CRA Net Worth Audits, Gross Negligence Penalties, and Tax Court Appeals

Similar evidentiary reconstruction principles apply in Canadian crypto tax audit disputes involving blockchain verification and exchange record analysis (see cryptotaxlawyer.com for related analysis).

What is a CRA net worth audit?

A CRA net worth audit is an indirect audit method used to estimate income based on changes in assets, liabilities, and expenditures rather than direct accounting records.

Why does the CRA use net worth assessments?

The CRA uses net worth assessments when it believes a taxpayer’s records are incomplete or unreliable.

Can CRA net worth assessments be challenged?

Yes. They are frequently challenged where assumptions regarding assets, liabilities, or expenditures are incorrect or unsupported.

Can a CRA net worth audit be successfully challenged in Canada?

CRA net worth audit can be successfully challenged in Canada where the CRA’s assumptions regarding income, assets, liabilities, or personal expenditures are inaccurate or unsupported by evidence. These audits are indirect and rely on reconstructing income based on changes in net worth rather than direct accounting records. As a result, they are highly sensitive to errors in opening balances, asset valuation, shareholder loans, and non-taxable sources of funds. In Tax Court of Canada appeals, taxpayers often succeed by providing banking records, accounting documents, and other objective financial evidence that contradicts the CRA’s assumptions and demonstrates a more accurate financial picture.

What evidence is most important in a CRA tax audit defence?

The most important evidence in a CRA tax audit defence is objective, contemporaneous financial documentation that independently verifies income and expenses. This typically includes banking records, corporate and personal tax returns, accounting ledgers, point-of-sale (POS) data, and third-party records such as franchisor or supplier reports. In CRA net worth audit cases, reconciliation between POS systems, bank deposits, and reported income is especially persuasive because it directly tests the CRA’s reconstructed income assumptions. The strongest defence evidence is consistent, verifiable, and capable of directly challenging the CRA’s indirect audit methodology.

Can gross negligence penalties be removed?

Yes. They may be reduced or eliminated depending on the facts and evidentiary record.

What is the role of a Canadian tax lawyer in a CRA audit?

A Canadian tax lawyer assists with evidence review, procedural strategy, dispute resolution, and Tax Court representation.

When should a taxpayer seek legal advice?

As early as possible, ideally at the start of a CRA tax audit or immediately upon receiving a reassessment.

CRA Tax Audit Take Away: Importance of an Experienced Canadian Tax Lawyer in CRA Net Worth Assessment Disputes

This case demonstrates that a CRA tax audit outcome is not predetermined.

TaxPage’s litigation strategy in this matter demonstrates how structured evidentiary development combined with procedural remediation can materially alter the outcome of CRA tax audit and Tax Court of Canada appeal proceedings.

Despite significant initial exposure, procedural deficiencies, and a substantial CRA net worth assessment, TaxPage was able to achieve a materially improved result through structured litigation strategy, evidentiary development, and targeted negotiation.

The final outcome included a reduction of taxable income from approximately $727,000 to approximately $310,000, elimination of gross negligence penalties exceeding $66,000, and total financial savings estimated at approximately $330,000.

This result underscores the importance of engaging an experienced Canadian tax lawyer or Canadian tax appeal lawyer early in the process to properly manage both evidentiary and procedural risks.

According to David J. Rotfleisch:

“A CRA tax reassessment is not the final word. With the right evidentiary foundation and legal strategy, many assessments can be significantly reduced or successfully challenged.”

Disclaimer: This article is provided for general informational purposes only and reflects the law as of the date of publication. It does not constitute legal advice and should not be relied upon as such. Tax situations are highly fact-specific and may vary significantly depending on individual circumstances. Readers facing a CRA tax audit, CRA net worth assessment, gross negligence penalties, or a Tax Court of Canada appeal should seek advice from an experienced Canadian tax lawyer.

Case Overview:

Jill (real name withheld due to solicitor – client confidentiality) is a resident of Ontario and owned one condo in downtown Toronto, and a bigger and more expensive home in the affluent community of Oakville, southwest of Toronto.

In 2022, Jill bought the condo and began actively splitting her time between the condo and her Oakville home. Jill, among various other reasons, used the condo to be closer to her friends and family, attend live entertainment including the ballet, watch local plays, and support her favourite hockey team at Scotiabank Arena.

The Problems & Our Approach:

1st Issue: Jill’s First Mistake

Jill filed the Vacant Home Tax Declaration (‘VHT Declaration’) in time and avoided having to pay the Vacant Home Tax (‘VHT’) for 2022. Inadvertently, she missed the deadline of February 29, 2024, to file her VHT Declaration for 2023. This was her first mistake.

In March of 2024, Jill sold the condo to Mr. and Mrs. Purchaser, who were both arm’s length purchasers from her. In the same month, the condo was deemed vacant by the City of Toronto (‘Toronto’) due to the failure of Jill to file a VHT Declaration for the 2023; and Toronto issued VHT assessment to Jill for a total amount of about $16,000.

In an effort to correct her omission, in April of, 2024, Jill filed a Notice of Complaint with Toronto (‘the complaint’) in order to have the Condo declared as occupied for the 2023 calendar year.

2nd Issue: Jill’s Second Mistake

Jill filed the complaint online through Toronto’s application portal. This complaint simply read as follows:

To whom it may concern

I recently filed in my vacancy tax form incorrectly. I lived there. I just have residences and go back and forth due to family issues.

Thank you,

Jill

Jill, in a hurry and thinking that this issue would be resolved quickly and easily, wrote and submitted this simple and short letter without providing proper details of her living situation and without any supporting documentation.

Worse, Jill decided against getting the help of skilled Canadian tax lawyers believing her problem was a trivial issue.

3rd Issue: Unconstitutional approach taken by the City of Toronto in handling this situation

In July 2024, Toronto Revenue Services Division, instead of issuing the letter to Jill who filed the complaint and who owned the condo in 2023, issued the decision letter addressed to Mr. and Mrs. Purchaser, current owners of the condo, notifying them that the complaint had been filed. The letter also asked Mr. and Mrs. Purchaser for additional supporting documents to confirm the occupancy status of the condo during the 2023 calendar year.

Further, the July letter also indicated that, as the condo had been purchased by Mr. and Mrs. Purchaser in 2024, that the new owners would not be eligible to file a notice of complaint themselves, but would be liable for the VHT assessed. This made Jill vulnerable to a potential civil lawsuit by Mr. and Mrs. Purchaser for the complete VHT.

4th Issue: Jill’s Third Mistake

When Jill received the July letter from Mr. and Mrs. Smith’s lawyer, Jill, once again wrote to the Toronto Revenue Services Division in August of 2024 stating that although the condo was not her ‘primary residence’, she lived there at least half of the year, if not longer.

Jill further stated that she has family in Toronto, her ex-partner, and friends and therefore, owned a second property. Finally, Jill stated that she did not rent the apartment nor was it vacant. To support her letter and her position, Jill attached her (1) property tax bill from Toronto and (2) Toronto hydro (electricity) bills for the condo for 2023.

Taxpage, after having a consultation with Jill, found out that when Jill wrote to the City of Toronto stating that the condo was not her ‘primary residence’, Jill was thinking in terms of her persoanfederal income tax exemption for her primary residence. Her obligations related to this new (VHT) municipal tax did not cross her mind.

Jill did not declare her condo as her principal residence in her income tax return for her principal residence exemption. She saved that for her Oakville house, which is much more valuable, but this did not negate the fact that she primarily stayed in the Toronto condo.

Furthermore, the property tax bills and electricity bills, although addressed to Jill, were delivered to Jill’s Oakville residence.

Lastly, in the eyes of the City of Toronto, Jill would have incurred property tax and bare minimum electricity bills even if she did not reside at her condo.

Because of lack of prima facie evidence, in September of 2024, Toronto rejected Jill’s second complaint and therefore decided that she was still liable for VHT. Once again, the City of Toronto provided no reasons to Jill and the decision letter was again delivered to Mr. and Mrs. Purchaser who had absolutely nothing to do with the filing of the complaint.

Jill Finally Seeks the Help of Canadian Tax Lawyers at Taxpage

In November of 2024, Jill hired Taxpage to help her out. Taxpage immediately filed a Freedom of Information request with the City of Toronto to obtain (1) all evidence and complaints submitted by Jill and; (2) internal notes of the city of Toronto, so that we could find out why Toronto was refusing to waive the VHT. No rationale was ever provided by the City of Toronto to Jill for their determination that she was liable for VHT.

By the beginning of December of 2024, we received the Freedom of Information package from the City of Toronto which provided Taxpage with some insight.

Now, because the deadline to file an administrative appeal was 90 days from the issuance of appeal and time was running out, the Canadian Tax Lawyers at Taxpage used the information package from the Toronto to immediately prepare and submit an appeal to Toronto and explained (1) why Jill stated that Condo is not her primary residence (2) and why the usage of Condo by Jill was enough in the eyes of the Toronto municipal law for it to consider the Condo as ‘ordinarily occupied’ in the eyes of the bylaw of Toronto.

Steps Taken by Taxpage to Resolve the Vacant Home Tax on Jill’s Condo

For supporting documents, Taxpage, in addition to electricity bills, attached:

- Home Internet and TV Bill

- Home Insurance Bill

- Email correspondence between Jill and her friends to coordinate gatherings at the condo

- Email correspondence between Jill and her property manager for general repair and upkeep of the condo

- Sales receipts for catering delivery to the condo

- Affidavits of Jill and her ex-partner attesting to Appellant’s use of the condo.

Despite submitting a detailed appeal and supporting documents, the City of Toronto still refused to waive the VHT. Furthermore, the City of Toronto, in all its wisdom, once again issued its decision letter in response to our appeal to the Real Estate Lawyer of Mr. and Mrs. Purchaser, which was forwarded to us after a month.

And to make matters worse, the City of Toronto once again provided no rationale for its determination and simply replied that Jill did not have enough evidence to prove her residence at the condo.

Taxpage Lawyers Talk to the City of Toronto’s Lawyers

Jill, on recommendation by Taxpage, decided to have us file a judicial review application of the City of Toronto’s decision with the Superior Court of Justice (Divisional Court) of Ontario (‘Div. Crt.’) as we had exhausted all administrative options to challenge the decision.

After filing the judicial review application, the Litigation Lawyer acting for the City of Toronto responded to our application and during the appeals process, Taxpage lawyersspoke directly to the City of Toronto’s lawyer, as is normal during litigation.

We explained our complete case to Toronto’s lawyer; that is, why Jill stated that condo is not her ‘primary residence’; provided valuation of Jill’s Oakville home to the lawyer (and to the Div. Crt. as well) and explained to him that because her Oakville home was way more expensive than the condo, it made sense for Jill to list her Oakville as her principal residence to claim her Personal Residence Exemption when filling her federal income tax.

We also explained to the City of Toronto Lawyer that their refusal to provide rationale for their decision made it hard for Jill (and for us at the Taxpage) to provide a proper submission to support her claim.

Result

Finally, the City of Toronto lawyer, well-versed in administrative law and constitutional law (unlike the Toronto Revenue Services Division), understood the complete issue (and foresaw the likely defeat of the City of Toronto at the judicial review hearing). He wisely decided to drop the $16,000 VHT levied against Jill’s condo just weeks before the application was scheduled to be heard in court.

Lessons Learned

Canadian taxpayers often make the wrong assumption that government officials on the other side, whether at the federal level (such as CRA) or provincial and municipal level, will be unbiased and well-versed in tax law. But the Canadian tax lawyers at Taxpage, often find that this is seldom the case.

Therefore, we always recommend that taxpayers get the experts involved to defend their rights from the very onset. As we see in this case, had Jill sought expert legal help in the beginning, the confusion of ‘primary residence’ would have never occurred. Moreover, Taxpage would have attached all important supporting documents from the very first submission.

Disclaimer: This case study provides information of a general nature only. It is only current at the posting date. It is not updated, and it may no longer be current. It does not provide legal advice, nor can it be relied upon. All tax situations are specific to their facts and will differ from the situations in the articles. If you have specific legal questions, you should consult an experienced Canadian Tax Lawyer.

Case Overview:

Taxpage has been tax counsel to clients, a married couple, whom we shall call Jack and Jill (names changed due to Solicitor – Client confidentiality) for the past 25 years. As part of our representation of Jack and Jill during all these years, we managed all their interactions with the Canada Revenue Agency (CRA). Please note that regardless of their marital status, Jack and Jill, like all Canadian taxpayers, are taxed individually and file separate tax returns in Canada.

In spring 2019, Jack and Jill were selected for a tax audit by the CRA’s Offshore Compliance Program. The CRA stated from the outset that this tax audit was to encompass only the years from 2010 through 2017.

Junior, the son of Jack and Jill, held a Swiss bank account through a trust. Junior and the trust are not Canadian tax residents. Over some years, Jack was a signing officer and potentially a Power of Attorney on the trust account.

The Problems & Our Approach:

1st Issue: CRA’s ‘Fishing Expedition’ and Taxpage’s tactics to stop it

In 2021, during the audit, Taxpage convened a conference tax audit interview with the CRA tax Auditor and her Team Leader. The attendees were (1) Mr. David Rotfleisch, Certified Tax Law Specialist and Chartered Professional Accountant (CPA) and Principal of Taxpage: (2) supporting tax lawyers, (3) the taxpayers being audited, and (4) officials from CRA.

During this meeting, the CRA Tax Auditor informally requested if there were any additional bank accounts held by Jack or Jill in the period from 2018 to present [2021]. Jill stated that she had an account briefly in 2019 at “Swiss Bank”. At the conclusion of the conference call, all participants, including Taxpage lawyers, agreed to forward, on an informal and voluntary basis (since the years being discussed were outside of the tax audit period) to the CRA on behalf of Jill, the statements from those accounts, which had already been closed. During the tax audit period as such, and up to the date of opening of Jill’s Swiss Bank account neither Jack nor Jill held any accounts at Swiss Bank.

As part of the tax audit, which became a fishing expedition at this point, the CRA sent a request to the Swiss Federal Tax Authority (Swiss FTA) requesting information and documents on any account held at the Swiss Bank for which Jack and Jill had a “Power of Attorney”.

Further, the CRA had made no such similar request related to powers of attorney to either Jack or Jill directly. This request from CRA did not name any specific 3rd parties. Moreover, this request by CRA to Swiss FTA was kept a secret from both Taxpage and Jack and Jill themselves. Taxpage was informed about CRA’s request to Swiss FTA via our trusted sources.

2nd Issue: CRA requested information that was improper and unlawful

During the tax audit or at any other time, the CRA has never requested from Taxpage any information related to any bank accounts or other property over which Jack and Jill have no beneficial interest, but merely a Power of Attorney or signatory power.

Had the CRA made such a request to us, we would have formally denied it, as in the opinion of Taxpage lawyers, it is clear from a Canadian income tax law perspective that such a request is improper and unlawful.

In fact, the Canadian tax lawyers at Taxpage had never seen such a request from CRA during their 40 years of practice.

Under Canadian tax law, a taxpayer is only required to report income and existence of any foreign property in accordance with the rules for reporting Specified Foreign Property (a defined term under the Canadian Income Tax Act) if the taxpayer is the beneficial owner of the same, regardless in which jurisdiction the property is situated. The 3rd party accounts on which a taxpayer merely holds a power of attorney or signatory power are taxwise irrelevant, and the respective bank information is thus not to be included in tax audit of the taxpayer.

As soon as Taxpage got to know that the request has been made by the CRA behind their backs to Swiss FTA, Taxpage immediately drafted a detailed letter to the Swiss Bank and informed them that any requests made to any party in relation to property in which Jack and Jill have no beneficial interest is improper and should be ignored or explicitly denied. In the letter, we further reiterated that no such request was made by the CRA to Jack and Jill directly.

In addition to notifying Swiss Bank about the rights of our clients, we also teamed up with a premier Swiss Law Firm expert in Swiss Tax Law in order to protect the interests of our clients. Taxpage provided the Swiss tax lawyers our Canadian legal analysis regarding the validity of the Request for Information (RFI) made by CRA to Swiss FTA.

Further, we at Taxpage informed the Swiss tax lawyers that if Swiss FTA proposes to release information about our clients Jack and Jill to CRA, Swiss tax lawyers would make a strong request to Swiss FTA to put the process on hold, pending resolution of an application (Writ of Mandamus) in the Federal Court of Canada to quash the entirety of the request on the basis of the patently false information set out therein.

Finally, the Swiss FTA, after the intervention of the Swiss tax law firm acting at the behest of Taxpage, refused to provide information about our clients Jack and Jill to CRA without Taxpage having to file the application to the Federal Court of Canada.

3rd Issue: CRA’S Offshore Compliance Program (OCP) kept the audit going for another 4 years

A reasonable person would think that 3 years would be more than enough time for Canada Revenue Agency to finish the audit. Various employees of the CRA working on the tax audit kept going on leaves of absence of more than 1 year, or retiring, while the file kept getting tossed from one auditor and team leader to another auditor and team leader.

Every time the CRA made a genuine request for more information and documents during the audit, we at Taxpage successfully provided the requested information and documents immediately in order to bring the audit to an end, but with every passing auditor, the CRA kept taking more and more time to respond to our emails and phone calls.

At this point, Taxpage and its clients, Jack and Jill, were unfortunately trapped in the bureaucracy. There is nothing that can be done to speed an audit along. Complaints and court applications will not achieve anything; , so we were going to waiting for this audit to end. But there was still one thing we could do.

Tax lawyers at Taxpage continued to follow up with the CRA to keep the pressure on them:

- we diarized follow-ups for the next few months;

- made phone calls from different phone lines because the CRA auditor stopped picking up our calls made from our usual phone lines;

- made irregular calls at odd times to catch the auditor off-guard.

The Result

Finally, in spring 2026, after 7 years, Taxpage received an audit completion letter from the CRA informing us that there was no problem in the tax filings of our clients. Because CRA’s ‘fishing expedition’ went nowhere, they decided to ‘cut bait.’ The Canadian tax lawyers at Taxpage got our clients, Jack and Jill, ‘off the hook’ completely.

Lessons Learned:

First, the CRA can and does chose Canadian Taxpayers for audit randomly. Therefore, Taxpage advises Canadian taxpayers to be very careful in filing their taxes; keep all bank records including in particular offshore bank accounts, sales records, receipts, invoices, and any other important paperwork in your possession for 10 years. It is better to get expert tax advice in the beginning when filing taxes so that in case the CRA audits you, your paperwork is complete. .

Second, CRA records every conversation during the tax audit, and the first conversation is the most important. A lot of Canadian taxpayers initiate the conversation with CRA officials and end up divulging potentially incriminating information and reach out to tax lawyers when it is too late. The best move is to always let an expert Canadian tax lawyer handle all communication with CRA officers from the beginning.

Third, the CRA can intrude on constitutional rights of Canadian taxpayers and has done so in the past. It is very important that Canadian tax lawyers are brought in to prevent the CRA from exceeding their executive authority.

Disclaimer: This case study provides information of a general nature only. It is only current at the posting date. It is not updated, and it may no longer be current. It does not provide legal advice, nor can it be relied on. All tax situations are specific to their facts and will differ from the situations in the articles. If you have specific legal questions, you should consult an experienced Canadian Tax Lawyer.

Case Overview:

The client was a self-employed musician who applied in good faith for a number of COVID-19 benefits released by the Federal Government of Canada, including the Canada Emergency Response Benefit (“CERB”) and Canada Recovery Benefit (“CRB”). The musician’s business was almost entirely halted due to COVID-19 lockdown restrictions on public performances.

The Canada Revenue Agency had initiated a review of the musician’s entitlement to those benefits. The musician’s benefits were denied at first review and second review because the musician purportedly failed to satisfy the minimum threshold of $5,000 in net income prior to the beginning of the COVID-19 pandemic.

However, the Canada Revenue Agency agents reviewing the musician’s case failed to provide a meaningful time to respond to requests and provided no reasons for rejecting the musician’s supporting documents showing at least $5,000 in net income during the relevant periods. The Canada Revenue Agency’s attempts to reach the musician were limited to a handful of phone calls.

The musician self-filed a Notice of Application for judicial review with the Federal Court, but mistakenly filed supporting evidence with those pleadings. The musician subsequently missed the deadline to serve supporting documents for that judicial review Application. Rotfleisch & Samulovitch was retained to bring the Application back on track, and to preserve the musician’s legal rights.

The Problem:

The Minister of National Revenue is granted the authority under law to verify an applicant’s eligibility for the CERB and CRB. If the Minister of National Revenue determines a person was not entitled to receive an income support payment, the Minister can choose to deny eligibility for those benefits. The Canada Revenue Agency exercises these powers on the Minister’s behalf.

Discretionary decisions of the Minister can be challenged by way of judicial review to Federal Court. With judicial review, the Federal Court is not responsible for reconsidering, reweighting, or reassessing information reviewed by a decision-maker. Rather, the Federal Court must evaluate if the decision made was reasonable after weighing the rationale provided by a decision-maker against available evidence. The Federal Court is also empowered to protect the procedural fairness of a review process. If a decision was unreasonable or a proceeding was procedurally unfair, the Federal Court can “quash” that decision, and send the case back for a redetermination. The Federal Court cannot make a decision for the Minister and can only require the Minister to reconsider the matter with additional guidance.

Judicial review is a fast process. Within 30 days of filing a Notice of Application, the Applicant must serve and file any affidavits and supporting evidence. Failing to meet any deadlines under the Federal Courts Rules can result in an Application being dismissed. And the right to extend deadlines is very limited.

Our Approach

Our Canadian tax litigation lawyers immediately contacted the Department of Justice Canadian tax lawyer assigned to our client’s file, and negotiated an extension of time to serve the client’s affidavit and supporting evidence.

We also undertook a thorough review of the client’s evidence, and filed a Rule 317 Request to obtain the full tribunal record reviewed by the Canada Revenue Agency agents who denied the client’s benefits. On reviewing those materials, it was discovered those agents had never actually contacted the client as suggested in their file notes. The client could produce phone records corroborating that phone calls purportedly made by the Canada Revenue Agency’s agents had never occurred, and that purported voicemails had never been left at the client’s phone number. While the evidentiary record at judicial review is usually constrained to what the decision-maker had available at the time, this evidence highlighted procedural defects not found in the tribunal record and was admissible.

We then immediately pushed for a settlement with the Department of Justice to have our client’s file sent back for a new review by an independent agent. We executed the Minutes of Settlement to obtain a new review, and filed a Notice of Discontinuance with the Federal Court shortly after, ending the Application.

The Result

The client’s file was sent back for a redetermination on its merits, with a new opportunity to submit supporting documents and to respond to further requests for information. In doing so, the musician was saved the full costs of a hearing before the Federal Court, while obtaining the exact remedy our client sought.

Lessons Learned

- Federal Court timelines for judicial review are unforgiving. Always make sure deadlines are met.

- The certified tribunal record is crucial for any judicial review case. The Federal Court rarely considers fresh evidence at a judicial review hearing. All supporting documents that can be submitted should be submitted on time during the initial review process to develop the tribunal record early.

- A hearing is not always required to win. Settlement can present a path to victory for a fraction of the cost.

- Do not undertake court proceedings without at a minimum advice from a tax lawyer and generally without fully retaining a lawyer to act on your behalf.

Case Overview:

A client retained Rotfleisch & Samulovitch to handle his TFSA related issue outstanding since 2016. The client had mistakenly overcontributed to his TFSA account and subsequently suffered significant losses in his TFSA investment account. As a result, the balance in his TFSA went down so much that the client had insufficient funds to withdraw the full excess contribution amount from his TFSA account. Further, the client has previously submitted a TFSA waiver request on his own, which was rejected by the Canada Revenue Agency. Due to the negative TFSA contribution room limit, the client continued to accrue interest and had no way to resolve the issue.

The Problem

The law A taxpayer’s TFSA contribution room is the maximum amount that a taxpayer can contribute to his or her TFSA account(s). Once the contribution room is used, withdrawals, excluding qualifying transfers and specified distributions, do not reverse the used contribution room. At any time in the year, if a taxpayer contributes more than his or her available TFSA contribution room, the taxpayer will have to pay a tax equal to 1% of the highest excess TFSA amount in the month, for each month that the excess amount stays in the taxpayer’s TFSA account(s).

A taxpayer is required to withdraw any excess contribution from his or her TFSA account(s) as soon as the taxpayer becomes aware of the issue, in order to qualify for relief via a TFSA waiver request. Other conditions must also be met for the relief to be granted by the CRA.

However, in the event that a taxpayer cannot withdraw the full amount of excess TFSA contribution due to investment loss, a taxpayer remains liable for the 1% tax of the highest excess TFSA amount in the month.

Normally, CRA takes the position that “only new TFSA contribution room that becomes available to the individual in future years will serve to reduce the excess TFSA amount.”

Our Approach:

We prepared and submitted a detailed second TFSA waiver request, including requesting a special one-time contribution room limit adjustment, asking the Canada Revenue Agency to allow an adjustment to the client’s TFSA contribution room limit, due to the client’s inability to remove the full amount of excess TFSA contribution. This is not an option set out or recognized by CRA. However, we made forceful arguments about the client being that it would be unfair to continue to penalize and charge the client a monthly tax indefinitely. As TFSA waiver request generally take several months to be processed, we actively followed up with the Canada Revenue Agency to have the client’s TFSA issue resolved as soon as possible.

The Result:

The client’s TFSA contribution room limit was adjusted to nil from -$125,561.91, once the TFSA waiver request has been accepted by the Canada Revenue Agency, saving the client over $4,000 in payable taxes and preventing any further monthly interest and penalties. The client also remained entitled to the annual increase of TFSA contribution room limit.

Case Issue

Our office was approached to represent an Ontario corporation (the “Corporation”) after its request for penalty and interest relief under the Canada Revenue Agency’s (“CRA”) Voluntary Disclosures Program was denied. The Corporation began operating in 2003, and earned significant income over the course of nearly two decades without filing any T2 corporate tax returns or GST/HST returns. The Corporation was involuntarily dissolved in 2007 for failure to file yearly information returns with the Ontario Ministry of Finance, but the Corporation’s proprietors continued to operate its business. The Corporation eventually filed a voluntary-disclosure application in 2020 under the CRA’s Voluntary Disclosures Program to correct its non-compliance issues.

The Corporation’s proprietors sought to administratively revive the Corporation after its voluntary-disclosure application was filed. These efforts were thwarted very quickly, however, because of errors on the part of the Ontario Ministry of Finance and the CRA. Specifically, the Corporation’s proprietors believed that the Corporation had a tax year-end that matched a calendar year-end of December 31. The proprietors prepared the Corporation’s tax returns on this basis. However, the Ontario Ministry of Finance and the CRA had each registered the Corporation with a different fiscal year-end. The Corporation therefore required the consent of the Ontario Ministry of Finance and the CRA to consolidate its three different tax year-ends, so that it could prepare and file its outstanding returns correctly for its voluntary-disclosure application.

The Corporation’s efforts were stonewalled by the CRA, who denied its initial request without any justification and subsequently took close to a year and a half to review and overturn its initial decision. The CRA subsequently ceased communicating with the Corporation and its representatives, while the Corporation’s proprietors and representatives continued to provide ongoing disclosure with respect to their efforts to revive the Corporation for its voluntary-disclosure application.

After nearly three years of silence from the CRA, it issued a letter concerning the Corporation’s voluntary-disclosure application. That letter requested the Corporation provide its articles of revival so that the CRA could continue to process its voluntary-disclosure application. That letter imposed a 15-day deadline to respond, and was sent exclusively by regular mail to the Corporation and its representatives. The CRA’s request was received late and was not replied to within the 15-day deadline imposed.

After receiving no response by the imposed deadline, the CRA quickly moved to deny the Corporation’s voluntary-disclosure application on the basis its application was incomplete. Curiously, that letter also stated the Corporation would not be entitled to apply for a second administrative review of the denial by an independent CRA decision-maker. And even more egregious, the decision letter stated that the Corporation’s right to judicial review of the CRA’s decision would be denied. As a result of CRA’s decision, the Corporation risked facing millions of dollars worth of penalties and interest, on top of the extensive tax debt it would owe after filing its outstanding returns.

Our office was engaged by the Corporation’s proprietors almost a month after the CRA’s decision to deny the Corporation relief under the Voluntary Disclosures Program, to determine if a solution could be found.

Approach

Our office immediately gathered all available evidence and filed an application for judicial review with the Federal Court of Canada. In that application, we argued that the CRA’s decision to deny the Corporation’s request for relief under the Voluntary Disclosures Program, and to deny the Corporation a second administrative review of that decision, should be set aside.

Our office argued that the CRA’s decision was unintelligible and that it deprived the Corporation of its rights to procedural fairness. The CRA’s decision regarding the Corporation was an administrative decision that affected the rights and privileges of the Corporation, and which attracted a duty of procedural fairness. Under the rules of procedural fairness, an adjudicator’s decision must be intelligible. Further, an applicant must have the right to make submissions and to present evidence.

Our office argued the CRA’s decision was a complete denial of natural justice and breached the Corporation’s right to procedural fairness in light of the principles above. First, the CRA’s letter imposed only a 15-day deadline to reply, and was issued by regular post. After nearly three years of silence from the CRA concerning the status of the Corporation’s voluntary-disclosure application, the Corporation was effectively ambushed with the CRA’s request, and which failed to provide the Corporation any meaningful opportunity to respond to its request for information. Second, the Corporation would have been unable to meet the CRA’s request for information in large part because of the inadvertence of the CRA itself. By denying the Corporation’s reasonable requests to have its tax year-end adjusted, the CRA itself had prevented the Corporation from being able to meet the CRA’s demands.

Third, and perhaps most egregious, was that the CRA’s decision explicitly denied the Corporation’s right to recourse. The decision letter denied the Corporation’s right not only to a second administrative review of CRA’s decision, but surreptitiously the Corporation’s right to file an application for judicial review. That right to file for judicial review is enumerated under section 18.1 of the Federal Courts Act, and the CRA had no right to deny the Corporation its statutory rights. The severe disconnect between the CRA’s reasoning and the outcome of its decision was untenable and rendered its decision wholly unreasonable.

Result

The CRA’s legal counsel at the Department of Justice engaged in settlement discussions with our office to resolve the Corporation’s judicial review prior to cross-examinations. The CRA consented to a settlement offer where the Corporation’s voluntary-disclosure application would be referred back for reconsideration, and the Corporation would be allowed to continue seeking its articles of revival. As a result, the avoided millions in penalties and interest owing for denial of relief under the Voluntary Disclosures Program, and its application was allowed to proceed on its merits.

Problem: Principal residence exemption denied

Rotfleisch & Samulovitch Professional Corporation represented a client who had been denied the principal residence exemption during a CRA income-tax audit.

The client had entered into an agreement to purchase the property in British Columbia a few years before the client was able to move in. Approximately six months after the property became available for possession, the property was sold after the client had resided at the property for four months. The client designated the property as the principal residence and filed a Principal Residence Exemption claim.

The CRA tax auditor initially intended to reject the client’s Principal Residence Exemption claim of $184,580 and added this amount to the client’s income in the original tax audit letter proposal.

However, as a result of the detailed tax submissions by our top Toronto tax lawyers the CRA tax auditor accepted the full Principal Residence Exemption claim.

Our Approach: Client was not a “house flipper”

Our experienced Canadian tax lawyers filed detailed submissions in response to the CRA tax audit to demonstrate that the property was intended to be the client’s principal residence and that the client was not in the business of “house flipping”.

Specifically, we argued that the relatively short period of time (i.e., four months) that the client resided in the property, prior to the sale of property, was due to unforeseen circumstances and health concerns.

The client’s intention to use the property as the principal residence should not be denied in consideration of the practical limitations. Therefore, the client should be entitled to claim the property as the principal residence.

Result: Complete tax victory over CRA

Our knowledgeable Canadian tax lawyers successfully defeated the tax audit without proceeding to the notice of objection stage. The CRA Audit Division adjusted its original proposal, reducing the client’s income by $184,580 (from $184,580 to nil) and allowing the full Principal Residence Exemption claim during the sale of the client’s property.

Client’s Situation:

Rotfleisch & Samulovitch PC, Canadian tax lawyers in Toronto, were retained by a property investor who intended to purchase a property that needed renovation. As a result of problems with the documentation, our client and her partners were assessed for HST in the amount of $459,286.

To raise funds, our client entered into a partnership agreement with four other individuals and purchased the property via a corporation created under the partnership’s ownership. Once the renovation was completed, the taxpayer decided to buy the property from the other four partners and made payments to each of them directly.

Challenges:

These partnership arrangements and documentation were all made without prior tax planning or consultation with a Canadian tax lawyer so the documentation of the transactions was inconsistent. The Agreement of Purchase and Sale between the taxpayer and her partners indicated the taxpayer

purchased the property from the corporation, while the Full and Final Release indicated the other four partners were the transferors. The CRA seized on these documentation inadequacies and then assessed the corporation for GST/HST on the sale of the property and reassessed the four other partners for the total amount of $459,286 under s.325 of the Excise Tax Act, which imposes joint and several liability for the unpaid GST/HST on the transferee where a person transfers property at less than fair market value on a non-arms length basis.

Our Approach:

Our experienced Canadian tax lawyers filed detailed notices of objection on behalf of the other four partners and made additional substantive and lengthy 52-page submissions in response to the appeals officer’s request to demonstrate that, despite the documentation inconsistency, the reality of the transaction was that the taxpayer only purchased the partnership and share interests from the other four individuals. Therefore, there was no taxable supply (sale in GST/HST language) hence no GST/HST should be owing.

The Result:

After three years and six months from the date we filed the notices of objection, the CRA finally allowed our objections in full and reversed the previous assessment for $459,286.

Case Issue

Our office was approached to represent a family trust (the “Trust”) following an incorrect audit undertaken by CRA’s Audit Division for the Trust’s 2013 to 2016 tax years. The Trust was a discretionary trust, and under the terms of the trust deed, the trustees were entitled to distribute any part or all of the Trust’s annual income and Trust capital at the trustee’s discretion to its beneficiaries (who were all the children of one of the trustees).

The Trust held dividend-paying shares in two very successful private Canadian companies. The Trust also earned business income by performing due diligence and management services for those companies and lending funds to them when necessary. From 2013 to 2016, the Trust earned substantial dividend income and business income from management fees. Further, in 2014, the Trust received payment back on a loan made to one of the companies, earning $3,000 in interest. And in 2015, the Trust sold shares in one company to an arm’s-length purchaser for substantial capital gains.

The Trust resolved (by way of a Deed of Distribution) in each tax year to allocate its income from each source fully to its beneficiaries. The Trust issued a demand promissory note to its beneficiaries totalling the income it had earned, rather than paying those amounts in cash. The Trust’s beneficiaries fully reported these amounts as personal income for their corresponding taxation years. These amounts were therefore deductible by the Trust under paragraph 104(6)(b) because they consisted of the Trust’s income “that became payable in the year to, or that was included under subsection 105(2) in computing the income of, a beneficiary.” As a result, the Trust had next to no taxable income from 2013 to 2016. In 2015, the Trust also elected to make a capital distribution of $50,000 to one beneficiary on a tax-free basis, which was made payable by way of a promissory note as well (and which was not included in any deed of distribution issued by the Trust).

Following an audit by CRA’s Audit Division, the CRA proposed and reassessed the Trust as follows:

- The auditor disallowed deductions that the Trust claimed under subsection 104(6) for: $32,234 in 2013; $19,500 in 2014; $60,000 in 2015; and $100,000 in 2016 (a total of $211,734). The auditor denied these deductions because, in his view, the demand promissory notes underlying these deductions failed to satisfy subsection 104(24), which deems an amount to not be deductible from a trust’s income unless the amount “was paid in the year to the beneficiary or the beneficiary was entitled in the year to enforce payment of it.” More specifically, the auditor compared the amounts that the Trust allocated to its beneficiaries with the Trust’s year-end bank balances. The auditor then concluded that subsection 104(24) precluded the Trust from claiming the deductions because the Trust did not maintain sufficient liquidity in its bank account to pay debts owed to its beneficiaries.

- The auditor disallowed a deduction of $41,744, which the Trust claimed for the 2014 taxation year, because the amount was paid to a non-listed beneficiary of the Trust (one of the trustee’s mother, who was not a beneficiary under the terms of the trust deed).

- The auditor assumed the $3,000 in interest income earned by the Trust was unreported dividend income, and included $4,140 in income for the Trust’s 2014 taxation year.

- The auditor disallowed a deduction for $50,000 claimed by the Trust in its 2015 tax year, on the basis the $50,000 payment to the Trust’s beneficiary could not have been a capital distribution, because the Trust’s opening and closing bank balance for 2015 were nearly identical.

By the time our office was contacted by the client, the trust’s accountant had already filed a notice of objection. Each argument presented in that objection had been flatly rejected by the CRA Appeals Division.

Approach

Our office immediately filed additional detailed submissions, and presented the following arguments to the CRA’s Appeals Division:

- The auditor had misunderstood and misapplied the terms of subsection 104(24), which does not deny a deduction under 104(6) if “the beneficiary was entitled in the year to enforce payment of [the amount deducted under 104(6)].” Rather, because the Trust had issued demand promissory notes, each recipient beneficiary “was entitled in the year to enforce payment of” the amounts that the Trust deducted, and so the amounts were fully deductible by the Trust because they consisted of the Trust’s income “that became payable in the year to a beneficiary.” The auditor had erroneously adopted a liquidity test and conflated the beneficiary’s entitlement to payment with the Trust’s ability to pay in a given year, which flew in the face of not only a plain reading of the statutes, but also case law and the CRA’s own published views on the subject.

- The $50,000 distribution made to a beneficiary of the Trust in 2015 was truly a capital distribution, and in effect the CRA intended to deny a deduction for a distribution by the Trust for which it did not otherwise claim a deduction. We demonstrated through analogy that the auditor’s assertion the Trust’s opening and closing bank balances alone were determinative of whether the Trust had made capital distributions was incorrect and a misapprehension of the law. Rather, by walking the CRA Appeals Division through the documentary evidence, we demonstrated that the capital distribution could be traced through the Trust’s bank balance. In fact, the auditor had arrived at the erroneous conclusion to disallow a deduction to the Trust because the auditor had actually mixed up two beneficiaries of the Trust, one of whom received a capital distribution (for which the Trust did not take a deduction) and the other who received an income distribution (and for which the Trust did take a deduction).

Result

The CRA Appeals Division agreed with our position and reversed the auditor’s decisions, reducing the Trust’s taxable income in 2013, 2015 and 2016 to almost nil. The Trust still recognized taxable income in 2014, in relation to distributions made to a non-beneficiary of the Trust that were erroneously deducted from its income, and for which there was no legal basis to dispute. In total, the CRA Appeals Division reduced the Trust’s taxable income by nearly $200,000 in total.

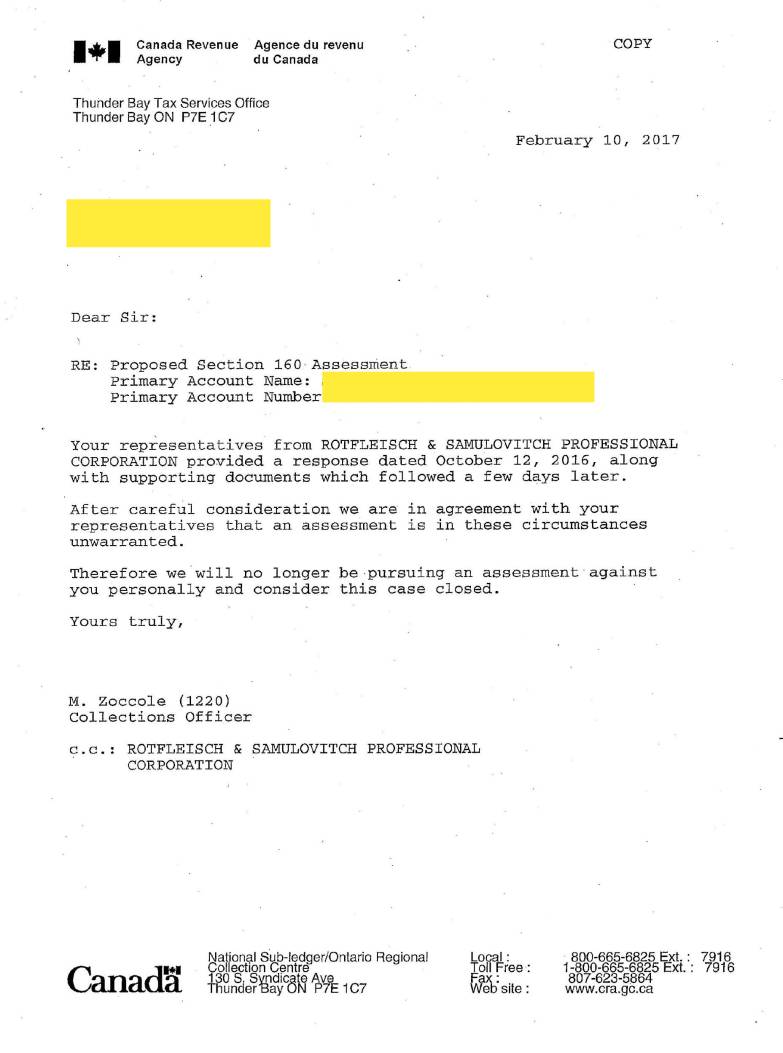

Case Issue

CRA’s Collections Division attempted to collect corporate taxes against a shareholder of a dissolved corporation. The collections officer examined bank statements of the corporation obtained directly from the bank and alleged non-arm’s length transfers and proposed to assess the client personally for the income taxes owed under section 160 of the Income Tax Act.

Approach

Our office conducted a line-by-line counter analysis and proved that the transfers were actually repayments of the shareholder’s loans to the corporation by paying legitimate business expenses using his personal credit card.

Result

CRA deemed the proposed assessment of $419,021.22 unwarranted and reduced it to $0 without doing any further evaluation.

{kind=link}

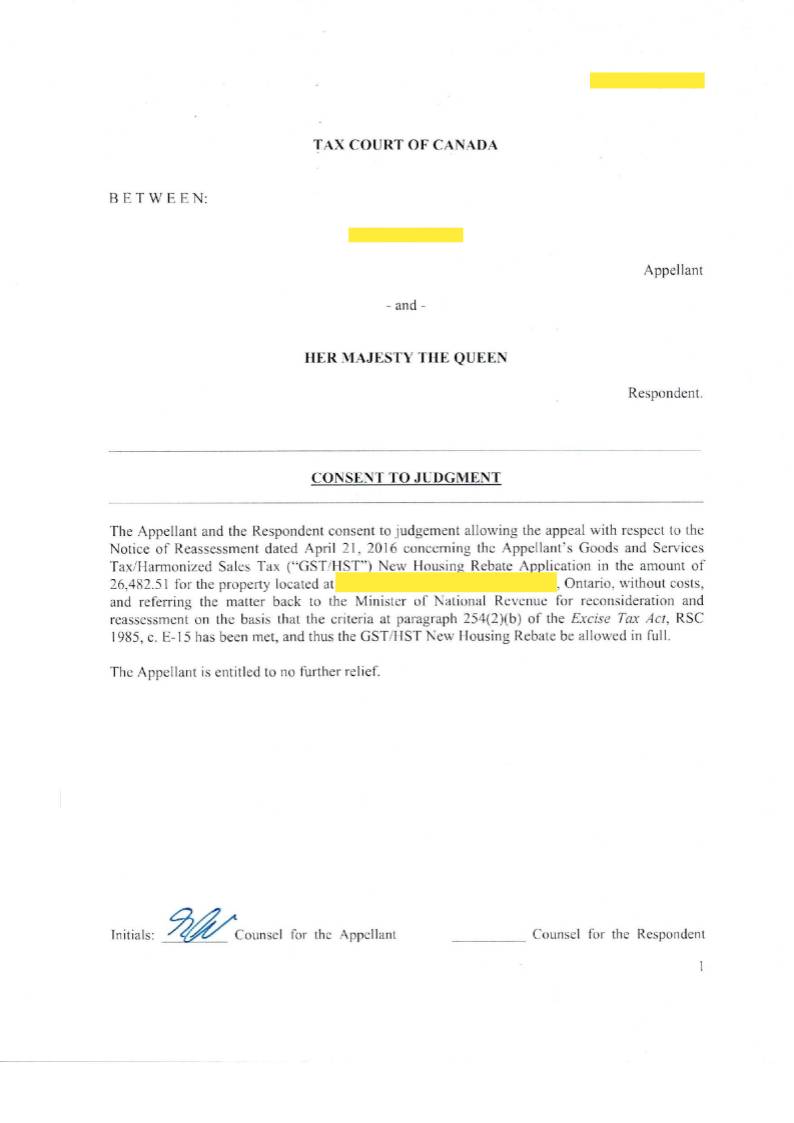

Case Issue

A client was reassessed and denied a previously paid HST new housing rebate.

Approach

We filed an informal-procedure Tax Court appeal on behalf of the client. While waiting for the hearing date to be set, we approached Crown with our theory and evidence of the case. Crown accepted our arguments and agreed to the appeal in full.

Result

The client saved $26,482.51 without the need to proceed to trial.

{kind=link}

{kind=link}

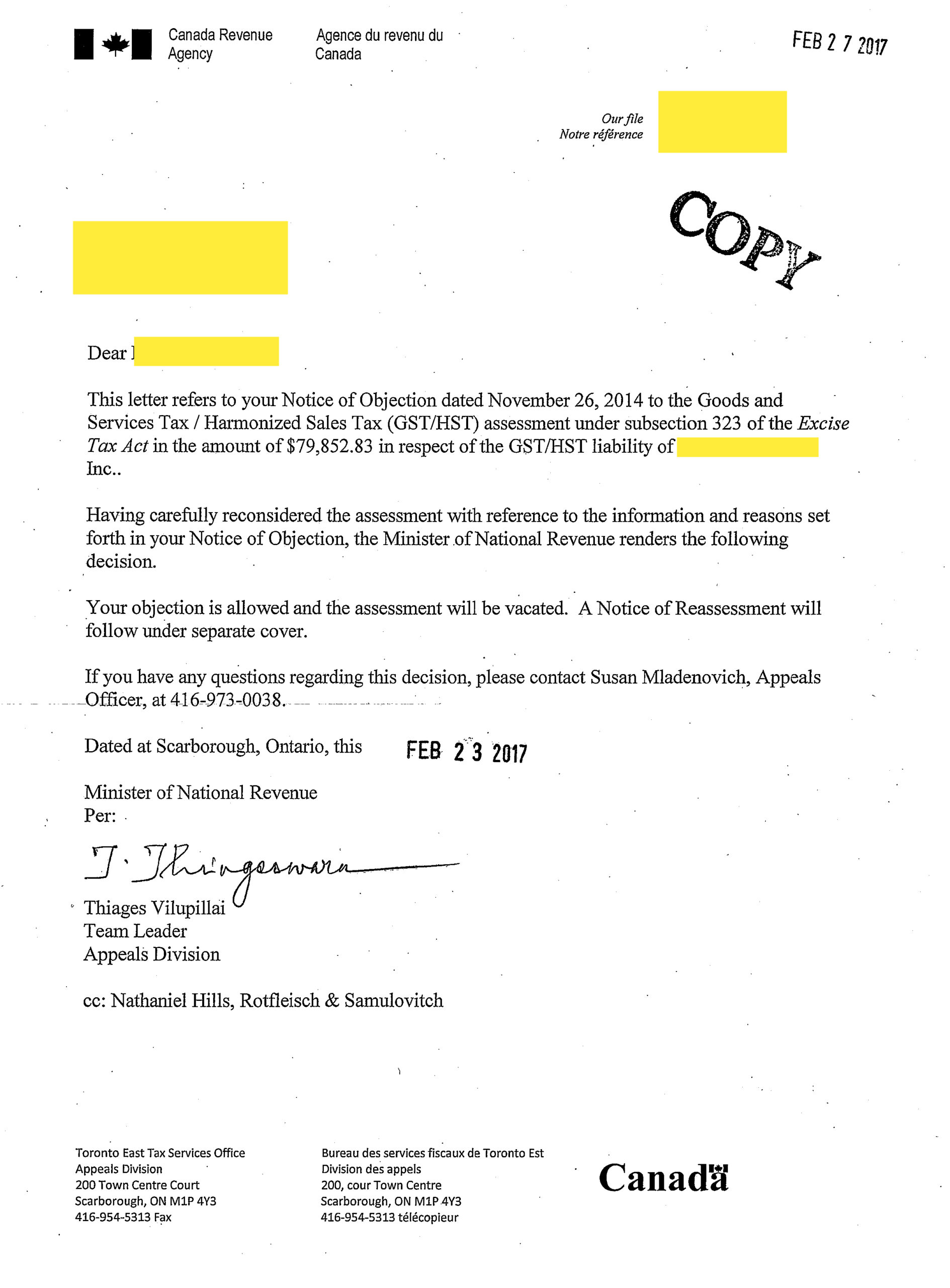

Case Issue

The client came to us to represent his corporation, locked out of its premises, pending a Goods and Services Tax/Harmonized Sales Tax (GST/HST) appeal in Tax Court. The books and records of the corporation had been seized, so the Canada Revenue Agency (CRA) assessed an arbitrary amount of $79,852.83 for the corporation’s GST/HST liability for the relevant period.

Approach

After going through the records, we discovered the client had been assessed personally as director of the corporation. We filed a notice of objection with the CRA on the basis that the director had been duly diligent in fulfilling the corporation’s tax obligations. The Crown agreed to put the Tax Court appeal of the corporation on hold until the CRA decides on the objection.

Result

The CRA allowed the objection and vacated the liability assessment of $79,852.83 for GST/HST without the need to proceed to expensive litigation.

{kind=link}

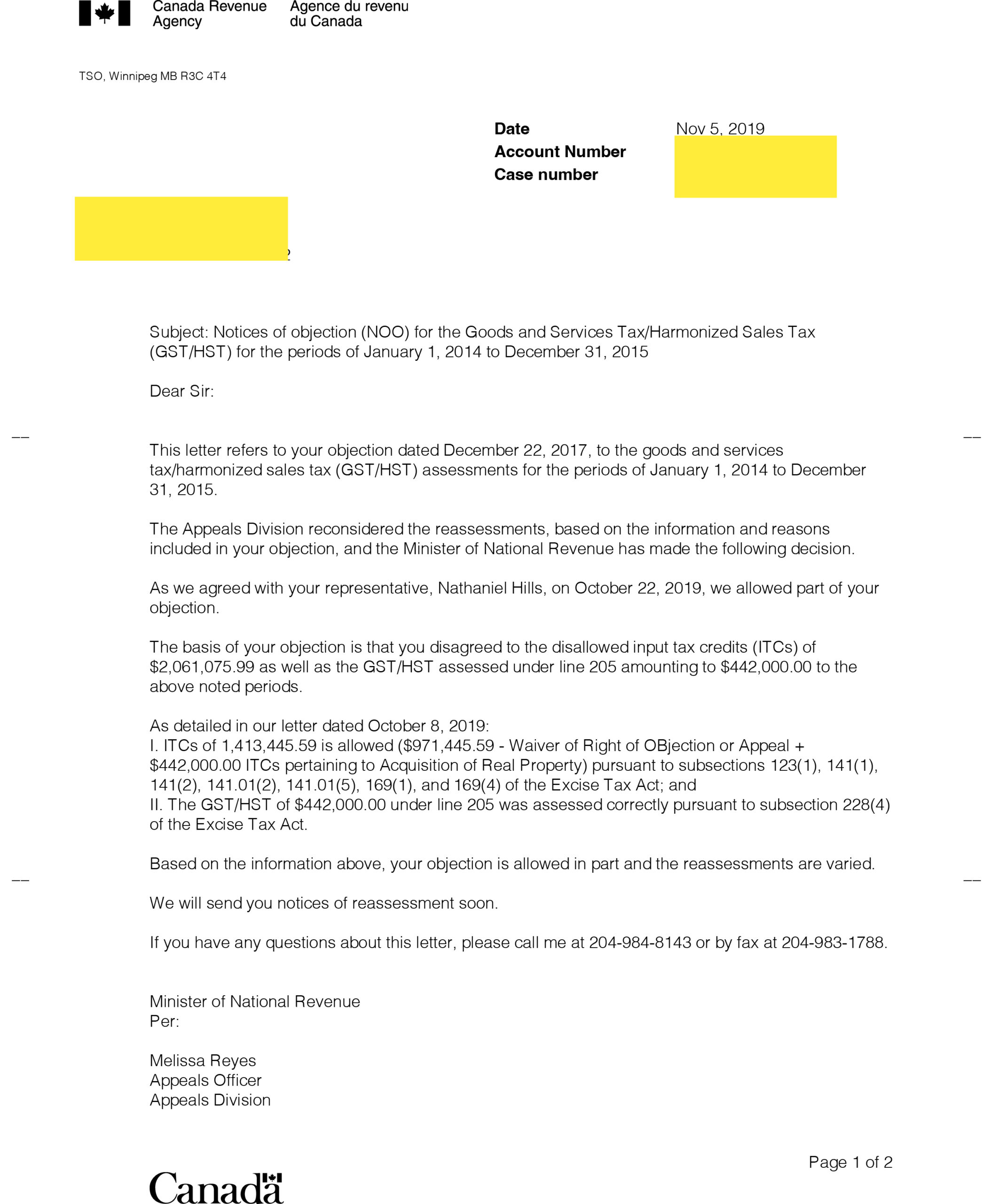

Case Issue

A client approached us to handle a denial of more than $1 million in input tax credit (ITC) refunds for the not-for-profit organization.

Approach

We sent a notice of objection to the Canada Revenue Agency, arguing that the disallowed ITCs involved legitimate businesses offering services to the public. The Appeals Division allowed the objection in part and reassessed the Goods and Services Tax/Harmonized Sales Tax (GST/HST) of the not-for-profit for the relevant period.

Result

The client received an ITC refund of $1,413,445.59 and was paid to the corporation.

{kind=link}

Case issue

A client approached Rotfleisch & Samulovitch P.C. and sought tax-planning advice about an imminent $1 million payout from a foreign pension.

Approach

Rotfleisch & Samulovitch P.C. recommended a payout structure allowing the client and the client’s ex-spouse to divide the pension per their separation agreement and qualify for the RRSP foreign-pension rollover under paragraph 60(j) of the Income Tax Act.

Result

By following Rotfleisch & Samulovitch P.C.’s advice, they each saved $250,000 in income tax—a total tax savings of $500,000.

Case issue

A husband and wife asked that we represent them during a CRA income-tax audit. As a result of our submissions, the income-tax auditor reduced the initial proposed taxable income by $145,000.

Approach

After the audit’s conclusion, we pursued the dispute with the CRA’s Appeals Division. So far, the appeals officer has agreed to reduce the couple’s taxable income by another $386,000 and cancel all $332,000 in gross negligence penalties.

Result

The objection remains active. But, to date, we have saved the couple from over $265,000 in taxes and $332,000 in gross-negligence fines. They got a total savings of about $597,000, plus a corresponding reduction to the interest previously accrued on the $597,000.

{kind=link}

Case issue

Alleging receipt of unpaid shareholder loans, the CRA increased our client’s taxable income by $567,000.

Approach

We filed a notice of objection, convincing the CRA appeals officer to reduce the amount by $61,500. We then filed a notice of appeal to the Tax Court of Canada. We secured an additional reduction of $373,000 during a pre-trial settlement with the Canada Revenue Agency and the Department of Justice.

Result

Our client’s taxable income was reduced by a total of $434,500.

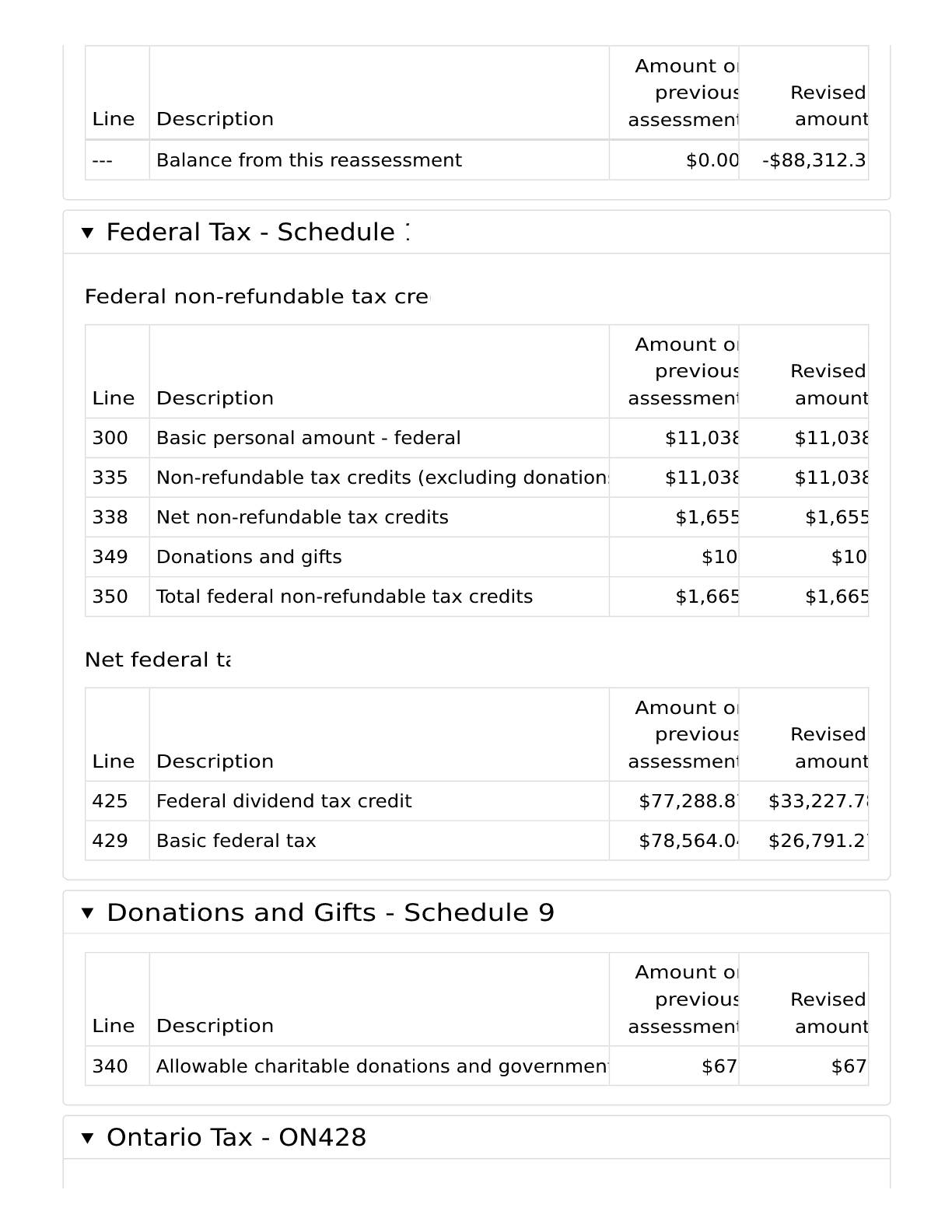

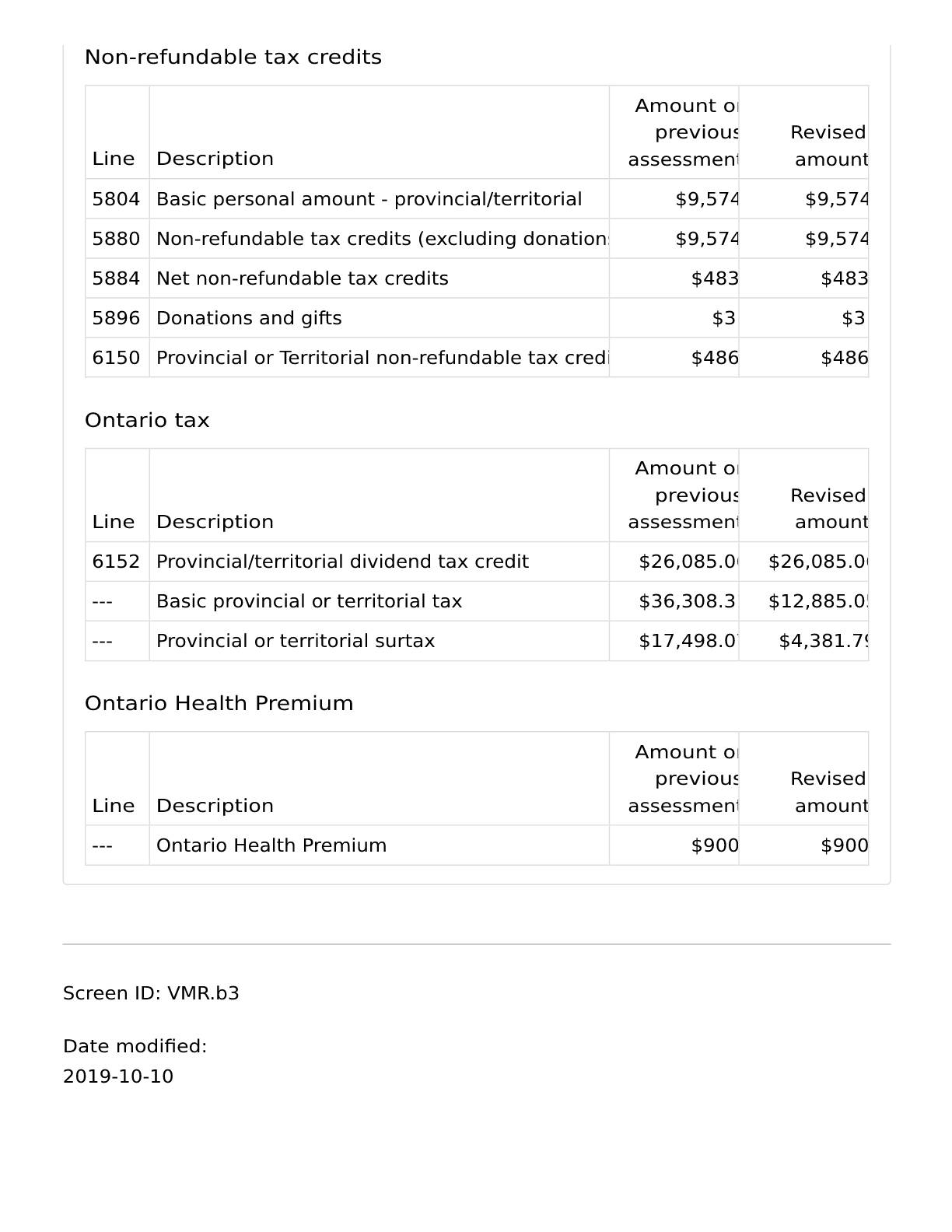

Case issue

The CRA had incorrectly reassessed the client for an additional $330,400 in taxable income. By the time the client approached Rotfleisch & Samulovitch P.C., he had exceeded the deadline to file a notice of objection or an extension-of-time application.

Approach

Still, Rotfleisch & Samulovitch P.C. managed to convince the CRA to reassess the impugned tax year yet again, thereby refreshing the deadline to file a notice of objection. The CRA appeals officer ultimately allowed the objection in full.

Result

The firm reduced the client’s taxable income by $330,400, and the client received an $88,000 tax refund.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Case issue