At a Glance: Current CRA Voluntary Disclosure Program Rules (2025–2026)

- The CRA Voluntary Disclosure Program (VDP) allows taxpayers to correct errors or omissions in their tax filings before the CRA takes enforcement action.

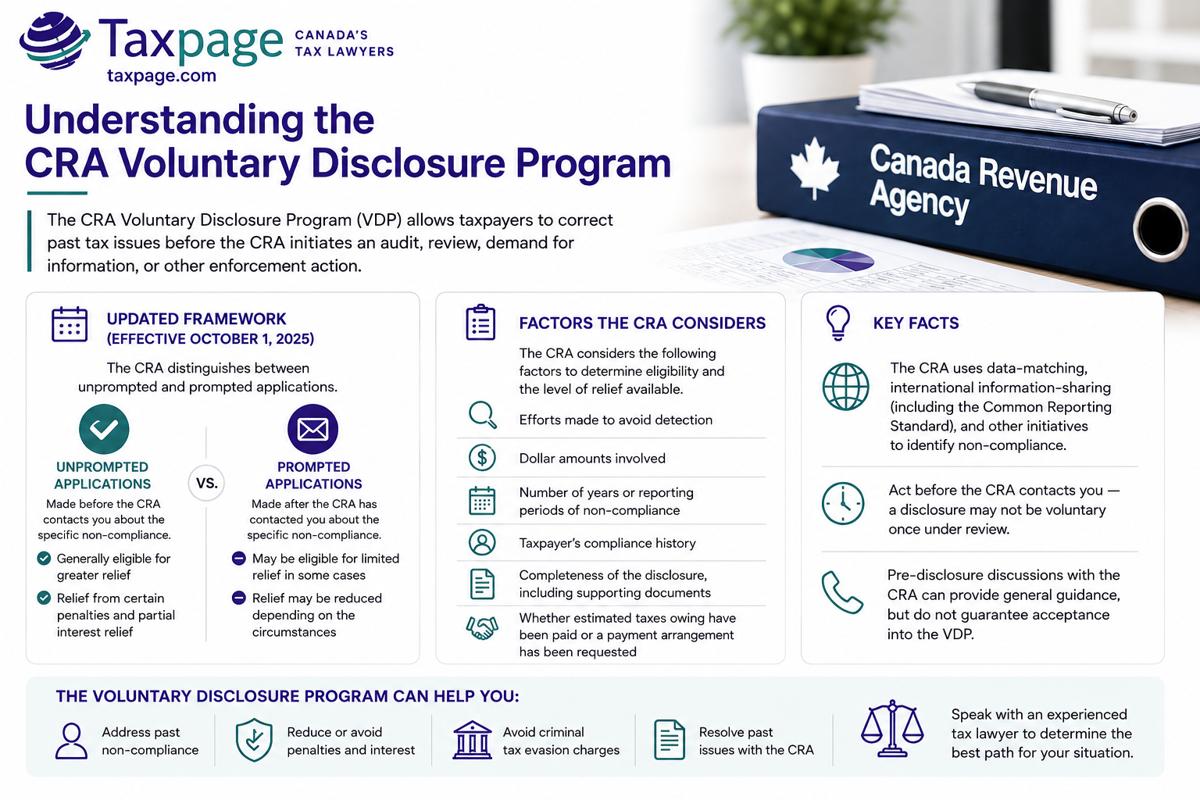

- For applications received on or after October 1, 2025, the CRA Voluntary Disclosure Program is administered under updated rules that distinguish between unprompted and prompted voluntary disclosure applications. The relief available depends on the timing of the disclosure, the nature of the non-compliance, the taxpayer’s circumstances, and whether the CRA has already contacted the taxpayer about the issue.

- In recent years, the CRA has increased its focus on identifying unreported income, undisclosed foreign assets, cryptocurrency transactions, and other forms of tax non-compliance through data-matching technology and international information-sharing agreements.

- Because eligibility for a voluntary disclosure depends heavily on timing, taxpayers should generally seek advice before the CRA initiates an audit, review, demand for information, or other enforcement action.

Work With Experienced Voluntary Disclosure Tax Lawyers

Taxpage provides quality tax solutions to individuals and businesses nationwide, including navigating Canada’s Voluntary Disclosure Program.

Our tax lawyers work with our clients to help them understand the eligibility criteria and application process to ensure they have the insight and resources they need to receive voluntary disclosure approval.

Learn how our VDP specialists can help you get started.

Understanding the CRA Voluntary Disclosure Program

The VDP, or Voluntary Disclosure Program, is a policy administered by the CRA that allows non-compliant Canadian taxpayers to come back into the tax system. Through the CRA Voluntary Disclosure Program, taxpayers can correct or amend previously filed tax returns, disclose information that was not previously reported to the CRA, and submit unfiled tax returns for prior years.

For CRA Voluntary Disclosure Program applications received on or after October 1, 2025, the CRA distinguishes between unprompted and prompted applications. An unprompted voluntary disclosure is generally made before the CRA has contacted the taxpayer about the specific non-compliance. A prompted voluntary disclosure may still be considered in some cases, but the relief available may be more limited depending on the facts.

The CRA may consider several factors when reviewing a VDP application, including:

- Whether the disclosure was made before CRA enforcement action;

- Whether the disclosure is complete;

- The dollar amounts involved;

- The number of years or reporting periods involved;

- The nature of the error or omission;

- The taxpayer’s compliance history;

- Whether the application includes supporting documents, and

- Whether the taxpayer has paid the estimated taxes owing or requested a payment arrangement.

Taxpayers considering a voluntary disclosure application should generally act before the CRA commences an audit, review, or enforcement action. Once the CRA has initiated contact about the issue, a disclosure may no longer qualify as unprompted, and the relief available under the Voluntary Disclosure Program may be reduced.

Taxpayers may still request pre-disclosure discussions with the CRA to obtain general guidance about the VDP process. However, pre-disclosure discussions do not guarantee acceptance into the CRA Voluntary Disclosure Program. Relief is only available once a complete voluntary disclosure application has been reviewed and accepted by the CRA.

Historical Note: Prior General Program and Limited Program Framework

Before October 1, 2025, the CRA Voluntary Disclosure Program operated under a General Program and Limited Program framework. Under that prior framework, taxpayers generally preferred acceptance under the General Program because it provided more favourable relief than the Limited Program.

For current VDP applications, taxpayers should focus on the updated prompted and unprompted application framework rather than the former General Program and Limited Program categories.

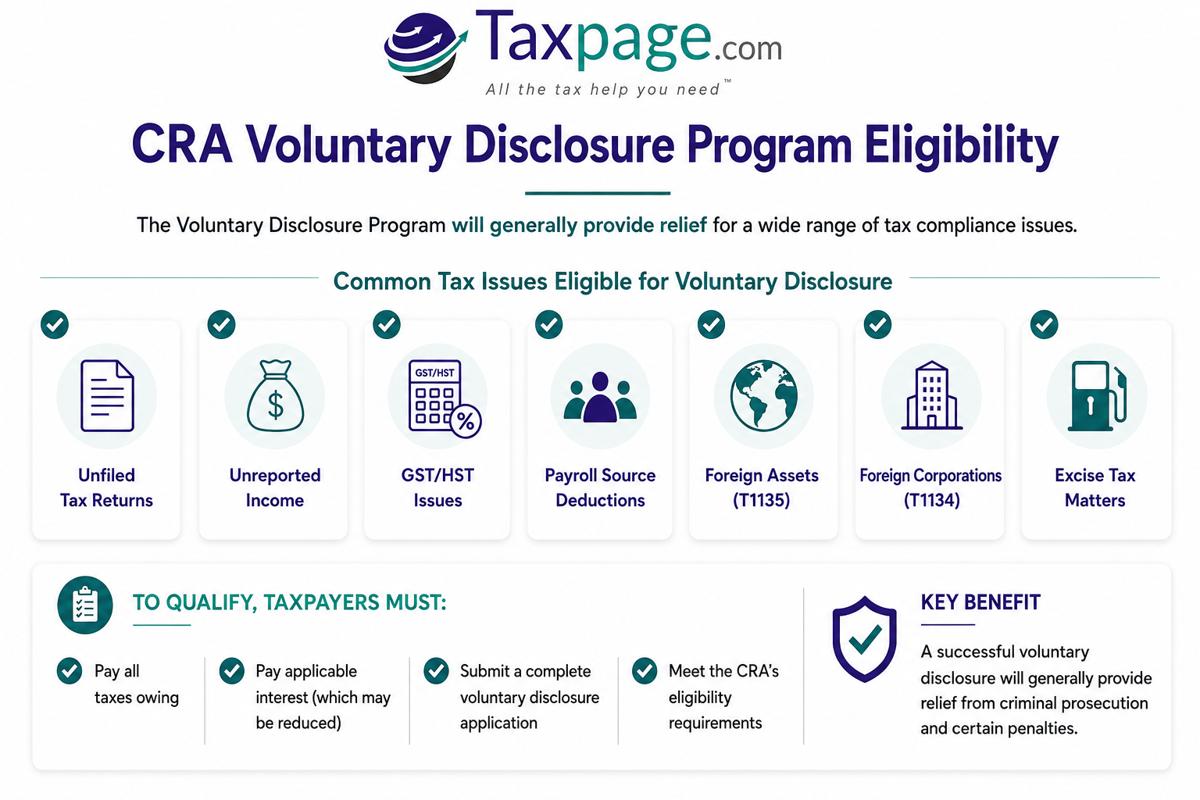

Voluntary Disclosure Program Disclosure Eligibility

The CRA Voluntary Disclosure Program may be available to taxpayers seeking to correct a variety of tax compliance issues. Eligible disclosures can include:

- Unfiled personal or corporate income tax returns

- Unreported income

- GST/HST reporting errors or omissions

- Payroll source deduction deficiencies

- Excise tax matters

- Undisclosed foreign assets and offshore income

- Information return filings, including Form T1135 and Form T1134

- Duties and obligations under various federal tax statutes

To receive relief under the CRA Voluntary Disclosure Program, taxpayers must still:

- Pay all taxes owing;

- Pay applicable interest charges (which may be reduced in certain circumstances);

- Submit a complete voluntary disclosure application; and

- Meet the CRA’s eligibility requirements.

One of the primary benefits of a successful voluntary disclosure application is relief from criminal prosecution and certain penalties that may otherwise apply.

Does The CRA Accept All CRA VDP Applications?

The CRA does not accept all Voluntary Disclosure Program applications in Canada. To qualify for relief under the current CRA Voluntary Disclosure Program, a taxpayer must submit a complete voluntary disclosure application that meets the CRA’s eligibility requirements.

For applications submitted on or after October 1, 2025, the CRA Voluntary Disclosure Program distinguishes between unprompted and prompted applications. An unprompted voluntary disclosure is generally one made before the CRA has contacted the taxpayer about the specific non-compliance issue. A prompted voluntary disclosure may still be considered in some circumstances where the CRA has contacted the taxpayer about a potential issue, but relief may be more limited depending on the facts.

To be accepted into the VDP, a voluntary disclosure application must generally:

- Be voluntary;

- Be complete;

- Involve an error or omission that may result in penalties, interest, or both;

- Relate to information that is at least one tax period past the filing due date;

- Include required supporting documents; and

- Include payment of the estimated taxes owing or a request for a payment arrangement.

Taxpayers must still pay any taxes owing. However, if a CRA voluntary disclosure application is accepted, the taxpayer may receive relief from certain penalties, partial interest relief, and protection from criminal prosecution for the matters disclosed.

The CRA reviews each VDP application on a case-by-case basis. Whether a taxpayer is accepted into the Voluntary Disclosure Program depends on the facts, the completeness of the disclosure, the timing of the application, and the nature of the non-compliance. Our experienced Canadian tax lawyers can prepare detailed submissions to help demonstrate that the CRA VDP requirements have been met and to maximize the taxpayer’s chance of obtaining relief under the current CRA Voluntary Disclosure Program.

Is There Any Time-Limit for Providing Information and Documentation for the Disclosure, So That the Application Is Not Rejected?

You’ll have a 90-day time limit. It begins with the EDD or the Effective Date of Disclosure. This is the day when the CRA has received the completed application submitted by your authorized Canadian tax lawyer.

You may ask for an extension in writing if you need it.

- Letter to Minister of National Revenue

- Response from Minister of National Revenue

Voluntary Disclosure beyond Ten Years

The CRA’s Voluntary Disclosure Program is currently governed by Information Circular IC00-1R7 for applications received on or after October 1, 2025. While the CRA may grant relief under the Voluntary Disclosure Program, certain forms of relief remain subject to a 10-year limitation period.

Tax years beyond the 10-year limitation period may still be relevant for several reasons.

- First, even when the source of a taxpayer’s non-compliance arose before the 10-year limitation period, the CRA may still grant relief for interest that accrued during the applicable relief period.

- Second, tax years beyond the 10-year limitation period may still be relevant to the completeness of a voluntary disclosure application. One of the requirements of the CRA Voluntary Disclosure Program is that the disclosure be complete. If a taxpayer’s non-compliance extends both within and beyond the applicable relief period, it is often advisable to disclose all relevant years to reduce the risk that the CRA will question the completeness of the application.

Because every voluntary disclosure application is reviewed on a case-by-case basis, taxpayers should seek professional advice when determining how many years of tax returns, information returns, and supporting documents should be included in their disclosure.

Voluntary Disclosure for Foreign Assets

While Canadian taxpayers are obliged to pay tax on the income generated from foreign assets, Canadian taxpayers are not taxed for owning assets overseas. However, through the T1135 form, Canadian taxpayers are required to disclose foreign assets when said assets are worth more than $100,000.00 Canadian dollars in value.

While Canadian taxpayers are generally required to report and pay tax on income earned from foreign assets, they are not taxed simply for owning property outside Canada. However, Canadian taxpayers may be required to file Form T1135, Foreign Income Verification Statement, when the total cost amount of specified foreign property exceeds $100,000 CAD.

Canadian taxpayers may also be required to file Form T1134 in connection with certain foreign corporations.

Failure to comply with foreign reporting requirements can result in significant penalties. As a result, taxpayers who have failed to report foreign income or file required information returns may be eligible to seek relief through the CRA Voluntary Disclosure Program.

The CRA receives information from foreign jurisdictions through international tax treaties, tax information exchange agreements, the Common Reporting Standard (CRS), and other international information-sharing initiatives. As a result, the CRA’s ability to identify undisclosed foreign assets and offshore income has increased significantly in recent years.

A voluntary disclosure application may allow taxpayers to correct failures relating to Form T1135, Form T1134, unreported offshore income, and other foreign reporting obligations before the CRA initiates an audit or enforcement action.

VDP Penalties

For CRA Voluntary Disclosure Program applications received on or after October 1, 2025, the relief available depends on the facts of the case and whether the application is treated as unprompted or prompted.

A successful VDP application may provide relief from certain penalties, partial interest relief, and protection from criminal prosecution for the matters disclosed. Taxpayers must still pay the underlying taxes owing and any interest that is not relieved by the CRA.

The CRA reviews each voluntary disclosure application on a case-by-case basis. Important factors include the completeness of the disclosure, the timing of the application, the taxpayer’s compliance history, the nature of the non-compliance, and whether the CRA had already contacted the taxpayer about the issue.

Historical Note: General Program and Limited Program Penalty Relief

Before October 1, 2025, the CRA Voluntary Disclosure Program operated under a General Program and Limited Program framework. Under the former Limited Program, relief was more restricted, and taxpayers could be required to waive certain objection and appeal rights for matters disclosed in the VDP application. That prior framework should now be treated as historical background for applications submitted before October 1, 2025.

Case Studies

Our Ontario tax law firm was contacted by John from Oakville, who had been charged with commercial fraud and had not reported the income from that fraud. We advised him that income from criminal activities is fully taxable and that the police always reported this type of activity to CRA. Our Toronto tax lawyers submitted a voluntary disclosure for the unreported income, and he was able to avoid prosecution for tax evasion and incurred no penalties.

Jeanne from Toronto approached our Canadian tax law firm on behalf of her mother, who resided in Montreal. Her mother had inherited 2 Swiss bank accounts, one with Swiss francs and the other with gold bars on the death of her husband. The bank accounts had not been reported to the CRA. The advice that our Toronto tax lawyers gave her was to submit, under the rules then in effect, no-name voluntary disclosures on behalf of the estate and her mother for unreported offshore income and unfiled T1135 offshore asset forms. We convinced CRA to limit the disclosure to the past 10 years. The tax department did not charge penalties and reduced the rate of interest charged on the unreported income.

C immigrated to Canada from Israel in the 1980s after working for a number of years in Africa and settling in Toronto. He had opened Swiss bank accounts to deposit his African earnings. He did not know that as a Canadian resident, he was required to report his worldwide income and offshore assets in excess of $100,000. He and his wife M also inherited a condo and funds in Israel. Our Canadian tax lawyers submitted an application on behalf of C and M and retained an accountant to prepare the tax returns and T1135 forms. We had extensive discussions with CRA about the number of years to file and persuaded them to limit the tax returns to 10 years. C and M did not have to pay any penalties and paid a reduced rate of interest on the unreported offshore income.

Robert is based in Manitoba but works overseas in the oil patch. His employer pays his foreign taxes, but his Canadian accountant did not properly report all of his foreign income due to the tax payments. Our Manitoba income tax lawyers submitted an application on his behalf and worked with his accountants to submit amended Canadian income tax returns. He avoided all penalties on the unreported offshore income and was charged a reduced rate of interest on the taxes owed.

Voluntary Disclosure Program: Tax Tips

Our experienced Canadian tax lawyers can help you understand what to expect when dealing with the CRA’s Voluntary Disclosure Program. We will assess whether you may qualify for relief under the CRA Voluntary Disclosure Program and help determine the most effective strategy based on your specific circumstances.

Our tax lawyers represent both individuals and businesses across Canada. We assist with voluntary disclosure applications, unfiled tax returns, offshore disclosures, GST/HST issues, payroll remittance problems, and other tax compliance matters.

Initial general email or phone responses are free. This is an opportunity to have your questions answered and better understand your options before taking action. All Taxpage consultations are completely confidential.

Find a VDP Expert

Taxpage is proud to be a trusted resource for tax planning, tax representation, tax garnishment, and voluntary disclosure in Canada.

We help individuals and businesses protect their legal rights and understand the complexities and nuances of Canada’s tax systems, including the CRA’s Voluntary Disclosure Program.

Contact a tax lawyer today to learn how to navigate a CRA voluntary disclosure form.